Budget Meaning and definition:

A budget, in a layman’s view, means an estimate of financial outflow in relation to financial inflow for a specific period. A budget is a breakdown of resources in a controlled manner to achieve the strategic objectives of an organisation in the short foreseeable future. In other words, a budget helps control the resources spent by an organisation to achieve its strategic objectives.

As per the definitions of various prominent institutes and economists, a budget may be defined as “a comprehensive statement of planned activities for a specific period, expressed in monetary and/or quantitative terms, prepared in advance to facilitate the efficient allocation of resources and to provide a framework for planning, coordination, and control of organizational operations.”

Hence, a budget is a very important control tool in the financial management of an organisation.

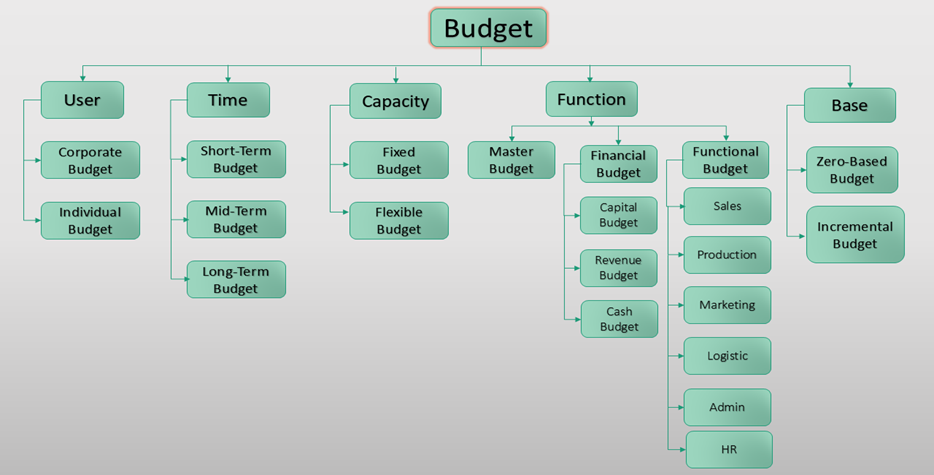

Categorization of Budgets in an organisation:

There are different types of budgets based on various parameters and requirements of the organisation. From auditors’ perspective the following categorization of budget would matter the most.

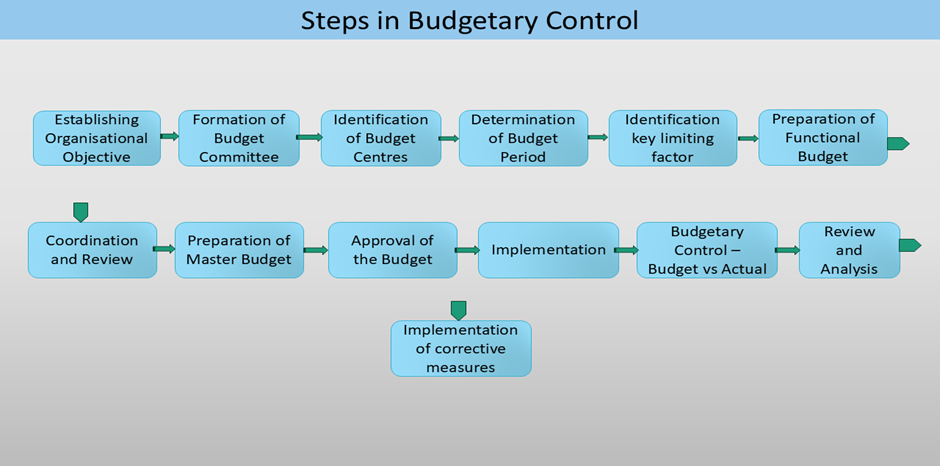

Budgeting Process:

Budget and Internal Audit:

The budget is an entity-level Internal Financial Control from an audit perspective. Prior to the commencement of an audit, the auditor should review the master budget and ensure the reasonableness of the items included in the budget. The basis and assumptions used in the preparation of the budget should be clearly documented as part of the budget document. The auditor should review the reasonableness of these assumptions and the basis used in preparing the budget.

Auditors should also review the minutes of Budget Committee meetings to gain an understanding of key business functions and the key controls exercised through the budgeting process in each function, based on the priorities assigned in the budget. Through this process, the auditor will also gain clarity regarding the strategic business objectives and the means adopted to achieve them.

At the engagement level, while performing planning and fieldwork, the auditor should review major deviations from the budget, assess the appropriateness of the reasons for such deviations, and verify whether proper approvals have been obtained. The auditor should also review the number of times the budget has been revised for the function under audit to evaluate the effectiveness of budgetary control.

– Thank you –