Introduction

The business environment today is characterized by rapid technological advancements, evolving regulatory requirements, increasing stakeholder expectations, and emerging risks that can materialize within days rather than months. Traditional internal audit methodologies, while effective in stable environments, often struggle to provide timely assurance and actionable insights in such dynamic conditions.

To remain relevant and value-driven, internal audit functions are increasingly embracing Agile Auditing-an approach inspired by Agile project management principles that emphasizes flexibility, collaboration, iterative execution, and continuous stakeholder engagement.

Agile Auditing does not alter the fundamental objectives of internal audit. Rather, it transforms the manner in which audits are planned, executed, and reported, enabling auditors to deliver assurance and advisory insights more quickly and effectively.

Meaning of Agile Auditing

Agile Auditing is a modern internal audit methodology that applies Agile principles to the audit process. Instead of conducting lengthy audits culminating in a single final report, Agile Auditing breaks the engagement into smaller, manageable phases or “sprints,” with frequent communication and incremental delivery of audit observations.

The key characteristics of Agile Auditing

- Iterative audit execution

- Continuous stakeholder collaboration

- Frequent communication of findings

- Flexibility to address emerging risks

- Prioritization of high-risk areas

- Faster delivery of audit value

In essence, Agile Auditing shifts the focus from “auditing at the end” to “providing assurance throughout the engagement.”

Key principles of Agile Auditing

- Focus on stakeholder value

- Prioritize high-risk areas

- Deliver findings incrementally

- Encourage continuous communication

- Embrace flexibility and adaptability

- Foster collaboration and transparency

- Promote continuous improvement

These principles help transform auditing from a periodic inspection activity into an ongoing value-adding function.

Why Agile Auditing is necessary in today’s audit environment

Rapidly changing risk landscape

Risks evolve continuously due to technological disruption, cyber security threats, regulatory changes, geopolitical developments, and changing business models. Audit plans prepared at the beginning of the year may become partially obsolete within a few months. Agile Auditing allows auditors to adjust audit priorities and scope in response to emerging risks.

Demand for timely insights

Management and boards increasingly require immediate visibility into control weaknesses and risk exposures. Waiting several months for a final audit report may delay corrective action.

Agile Auditing facilitates early communication of observations, enabling management to respond promptly.

Digital transformation

Organizations are adopting automation, cloud computing, artificial intelligence, and advanced analytics at an unprecedented pace. Internal audit functions must keep pace with these changes through more adaptive audit approaches.

Enhanced stakeholder expectations

Stakeholders no longer view internal audit solely as a compliance function. They expect practical recommendations, business insights, and proactive risk identification.

Agile Auditing promotes greater collaboration between auditors and business leaders, thereby enhancing audit relevance and value.

Resource optimization

Internal audit departments often operate with limited resources. Agile methodologies help focus audit effort on the most significant risks and control areas, maximizing value delivered per audit hour.

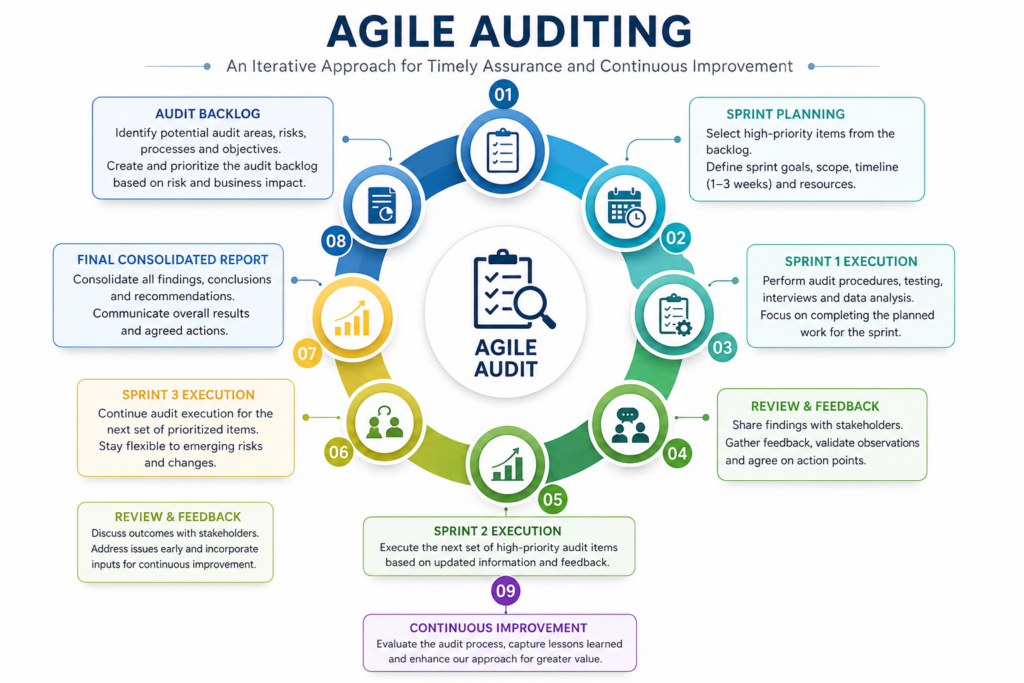

Steps in an Agile Audit Engagement

Step 1: Audit backlog creation – The audit team identifies potential audit areas, risks, processes, and objectives. These items are compiled into an audit backlog and prioritized based on risk and business significance.

Step 2: Sprint planning – The engagement is divided into short execution cycles known as sprints, typically lasting one to three weeks. Each sprint includes: (i)Defined objectives (ii) Scope boundaries (iii)Assigned responsibilities (iv)Expected deliverables

Step 3: Sprint execution – Auditors perform testing, interviews, walkthroughs, and analysis within the sprint period. The focus remains on completing and validating high-priority audit areas rather than attempting to review everything simultaneously.

Step 4: Daily or frequent team coordination – Short team meetings help: (i) Monitor progress (ii) Resolve obstacles (iii) Reallocate resources where necessary (iv) Maintain alignment with audit objectives

Step 5: Continuous stakeholder engagement – Findings are discussed with process owners as they emerge. This approach: (i) Reduces surprises (ii) Encourages prompt corrective actions (iii) Improves management buy-in

Step 6: Sprint review – At the end of each sprint, the audit team presents completed work and preliminary observations to stakeholders. Management receives actionable insights without waiting for completion of the entire audit.

Step 7: Sprint retrospection – The audit team evaluates: (i) What worked well (ii) What challenges were encountered (iii) Opportunities for improvement. This fosters continuous enhancement of audit quality and efficiency.

Step 8: Final consolidated reporting – After all sprints are completed, observations are consolidated into a final report summarizing key risks, findings, recommendations, and management actions.

Benefits and Drawbacks of Agile Auditing

Benefits of Agile Auditing

- Faster Delivery of Audit Results – Observations are communicated as they arise, allowing management to take corrective action sooner.

- Greater Audit Relevance – Audit focus can be adjusted when new risks emerge during the engagement.

- Improved Stakeholder Relationships – Frequent interaction fosters trust, transparency, and collaboration between auditors and management.

- Reduced Reporting Delays – Issues are resolved continuously rather than accumulating until the end of the audit.

- Enhanced Risk Coverage – Agile Auditing enables internal audit to focus on the most critical and evolving risks.

- Better Team Productivity – Short, focused work cycles improve accountability, visibility, and resource utilization.

- Increased Audit Value – Management receives actionable insights more quickly, strengthening the perception of internal audit as a strategic partner.

Drawbacks and Challenges

- Cultural Resistance – Organizations accustomed to traditional auditing may initially resist frequent interactions and iterative reporting.

- Scope Management Challenges – Without disciplined governance, audit scope may continuously expand due to emerging stakeholder requests.

- Increased Stakeholder Time Commitment – Frequent discussions and reviews require active participation from management.

- Training Requirements – Audit teams must develop new skills related to Agile methodologies, facilitation, communication, and adaptive planning.

- Documentation Discipline – Auditors must ensure that the flexibility of Agile does not compromise documentation quality and compliance with professional standards.

- .Not Suitable for Every Audit – Certain regulatory, compliance, or highly structured audits may still benefit from traditional audit approaches.

Practical Experience and Observations

From practical experience, Agile Auditing delivers the greatest value in environments characterized by rapid change, digital transformation, project implementation, and evolving operational risks.

Organizations often discover that the most significant benefit is not faster reporting but improved stakeholder engagement. Frequent interaction helps management understand risks more clearly and enables auditors to gain deeper insights into operational realities.

However, successful implementation requires more than simply dividing an audit into sprints. It demands a cultural shift toward collaboration, transparency, and continuous communication. Audit leaders must strike a balance between agility and professional rigor to ensure compliance with internal audit standards while maintaining flexibility.

In practice, the most effective audit functions often adopt a hybrid model, combining Agile techniques with traditional risk-based audit methodologies.

Conclusion

Agile Auditing represents a significant evolution in the internal audit profession. As organizations navigate increasingly complex and fast-changing business environments, the need for timely, relevant, and actionable assurance has never been greater.

By embracing iterative execution, continuous stakeholder engagement, and adaptive planning, Agile Auditing enables internal auditors to deliver insights faster, respond more effectively to emerging risks, and create greater value for organizations.

While implementation challenges exist, the benefits generally outweigh the drawbacks when supported by strong governance, appropriate training, and a culture of collaboration. Internal audit functions that successfully adopt Agile principles are better positioned to serve as trusted advisors and strategic partners in today’s dynamic business landscape.

~ Thank You ~