As governance evolved from monarchies to modern corporations, its core principles—structured authority, accountability, and informed oversight—remained constant, even as institutions became more complex. The shift from state administration to corporate enterprise required a formalized framework to manage dispersed ownership, professional management, and expanding stakeholder expectations. It is within this historical progression that modern corporate governance emerged, translating centuries-old governance principles into structured systems suited to contemporary organisations and regulated market environments.

Governance, as defined by the IPPF Standards, is the “combination of processes and structures established by the Board to inform, direct, manage, and monitor the activities of the organisation to achieve its objectives.”

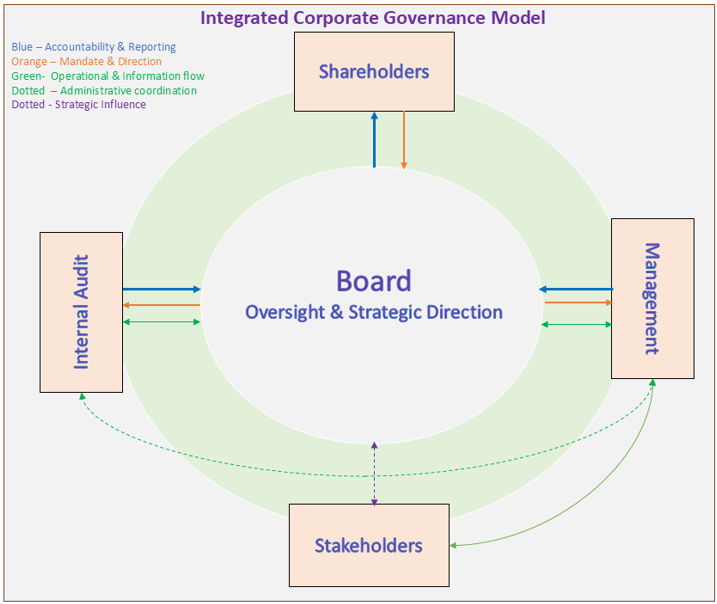

In simpler terms, governance functions like the central nervous system of an organisation. The Board serves as the “brain,” setting direction and providing oversight, while the various organisational structures act as connected components that implement those directions and continuously relay feedback to the Board. Within these structures, processes consist of coordinated actions and steps designed to achieve the organisation’s objectives effectively and efficiently.

As per the Organisation for Economic Co-operation and Development (OECD) “Corporate Governance involves set of relationship between a company’s management, its board, shareholders, and other stakeholders. Corporate governance provides the structure through which the objectives of the company are set and the means of attaining those objectives and monitoring performance are determined.”

The Board acts as the representative of the shareholders. Management is the organizational structure established by the Board to run the company’s day-to-day operations. Stakeholders are the individuals and entities affected by the organization’s activities. They include shareholders, employees, suppliers, customers, the surrounding community, and government regulators. Internal control is an integral component of the governance framework. Internal audit, on the other hand, is an independent function that evaluates the effectiveness of governance processes and provides appropriate recommendations to enhance and improve those processes.